Means Test Summary - (April 1, 2024 Standards)

[=] Your Means Test Data Summary

Your Income vs. Median Income

Assumptions about Your Situation:

- Marital/Filing Status:

- State:

(based on the zip code you're using) - Household Size:

(Form 22A-1, Line 13)

Median Income For Your Location (Form 22A-1):

- Median Income for

a person

household:

$0 per month ($0 annual)

(Form 22A-1 Line 13) - Your income for Median Income test:

$0 per month ($0 annual based on 6-month avg)

(Form 22A-1 Line 11, 12) - You are currently BELOW the median income for a person household.

Your Expenses & San Luis Obispo County Expense Standards

Expense Deduction Allowances For San Luis Obispo County,

(Form 22A-2):

Assuptions about your situation

- Number of Dependents for Expenses: (Form 22A-2, Line 5)

- Vehicles:

- on which you pay operating expenses: (Form 22A-2 Line 11)

- on which you pay ownership or lease expenses: (Form 22A-2 Line 11)

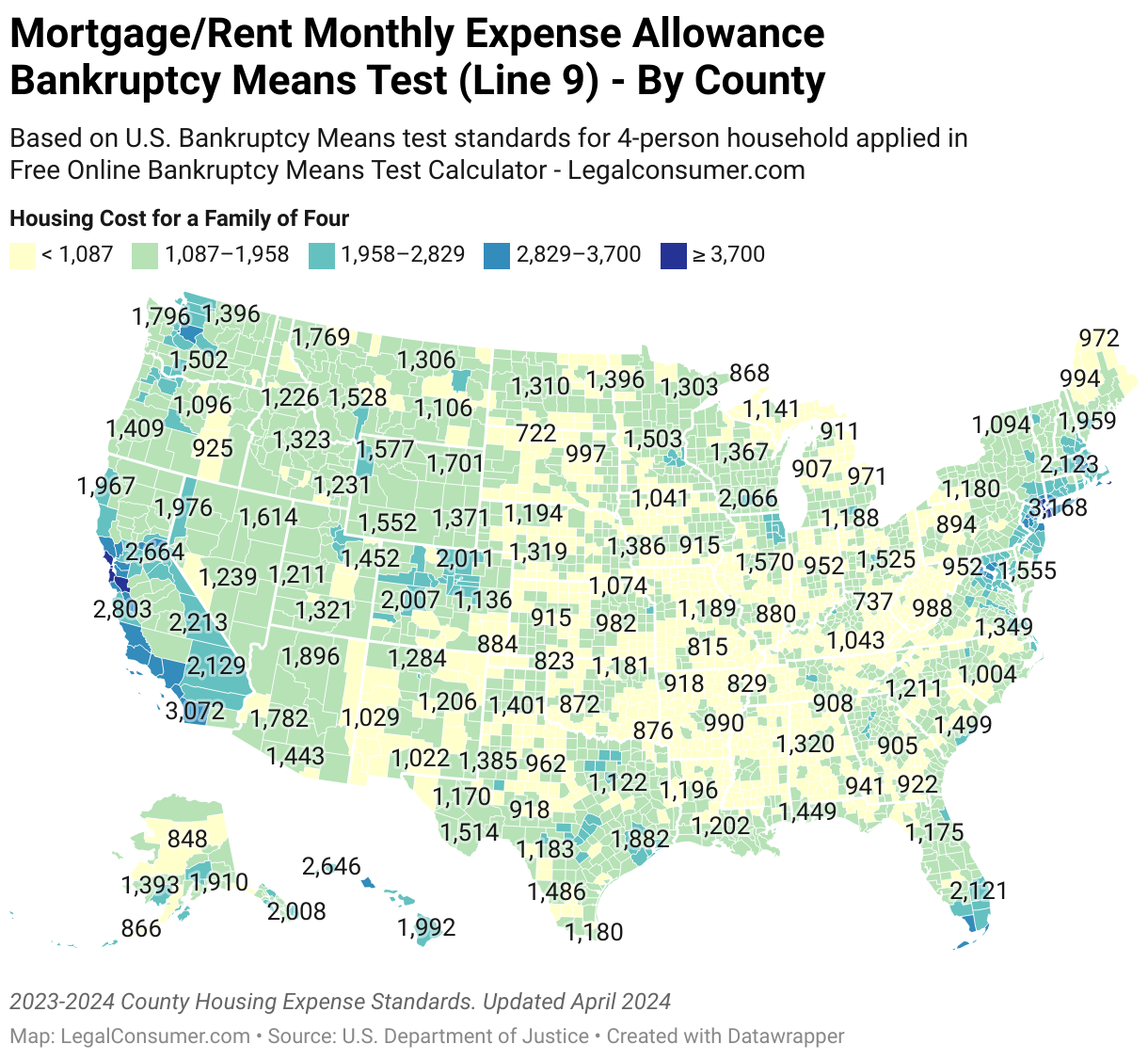

Housing expenses (Line 8 and Line 9

for persons in San Luis Obispo County, .

for persons in San Luis Obispo County, .

- $0 monthly expense allowance for housing and utilities, non-mortgage expenses (Line 8)

-

$0 monthly

expense allowance

for mortgage/rent expenses (Line 9)

(This is a minimum amount. if your mortgage payment is higher, you get the full amount of the mortgage.Not so for rent, unfortunately.)

Living expenses (Line 6)

-

$0 monthly

allowance

for food, clothing, household supplies, personal care, miscellaneous (Line 6)(Source:

National Standards (for -person households, regardless of income.)

Out-of-Pocket Healthcare expenses (Line 7)

- $0 monthly allowance for 'out-of-pocket healthcare costs' other than health insurance

- (Source:

National Standards for

* persons under 65

@$75/person and

* persons 65 or over

@$153/person.

See Line 7)

- $0 monthly allowance for vehicle operation expenses (i.e. gas, repairs, maintenance) for vehicles in West Region

- $ 0 additional monthly allowance claimed for public transportation (Line 15)

- $ 0 monthly allowance for vehicle ownership or lease expenses for vehicles . (This is the standard amount. If your car loan payment is higher, you can deduct the full amount of the car loan. Not so for lease expenses, unfortunately.)

Transportation expenses

Your Disposable income

Your Means Test Summary

Your Household Info

Marital/Filing Status:

(Form 22A-1, Line 1)

State:

(based on the zip code you're using)

County: San Luis Obispo County

(based on the zip code you're using)

Household Size:

(Form 22A-1, Line 13)

Number of Dependents:

(Form 22A-2, Line 5)

Number of Vehicles you maintain:

(Form 22A-2, Line 11)

Persons under 65 for whom you pay healthcare:

(Form 22A-1, Line 7)

Persons over 65 for whom you pay healthcare:

(Form 22A-1, Line 7

Median Income Test

![]() monthly median for a

-person

household:

$0

($0 annual)

monthly median for a

-person

household:

$0

($0 annual)

Your monthly household income

$0

($0 annual) (line

11)

Means Test

Monthly Income for Means Test

Monthly income for means test: $0 (Line 4)

Monthly Expenses

![]() Automatic

& Actual Deductions for San Luis Obispo County: $0 (Line 24)

Automatic

& Actual Deductions for San Luis Obispo County: $0 (Line 24)

Other Deductions (for Actual Expenses): $0 (Line 31)

Deductions for Debt Payment

$0 (Line

37)

TOTAL DEDUCTIONS:

$ 0 (Line

38)

Disposable Income (Line 39)

$

0 per month

($0 over 5 years)

Your Bottom Line

You must have your browser's cookie functionality turned on to use the calculator.

Based on the information you have entered so far, your monthly income of $ 0 is above the median for -person households in ($ 0), but you pass the means test because your expenses will leave you with disposable income of less than $136.25 per month and therefore amount to less than $9,051 over the next five years.

Summary of your data:

Your average monthly income is $0 and, so far, you have expense deductions totaling $ 0 per month. That would leave you with $ 0 at the end of each month to pay into a hypothetical, five-year Chapter 13 bankruptcy plan, which would pay your unsecured creditors $ 0 over the next five years.