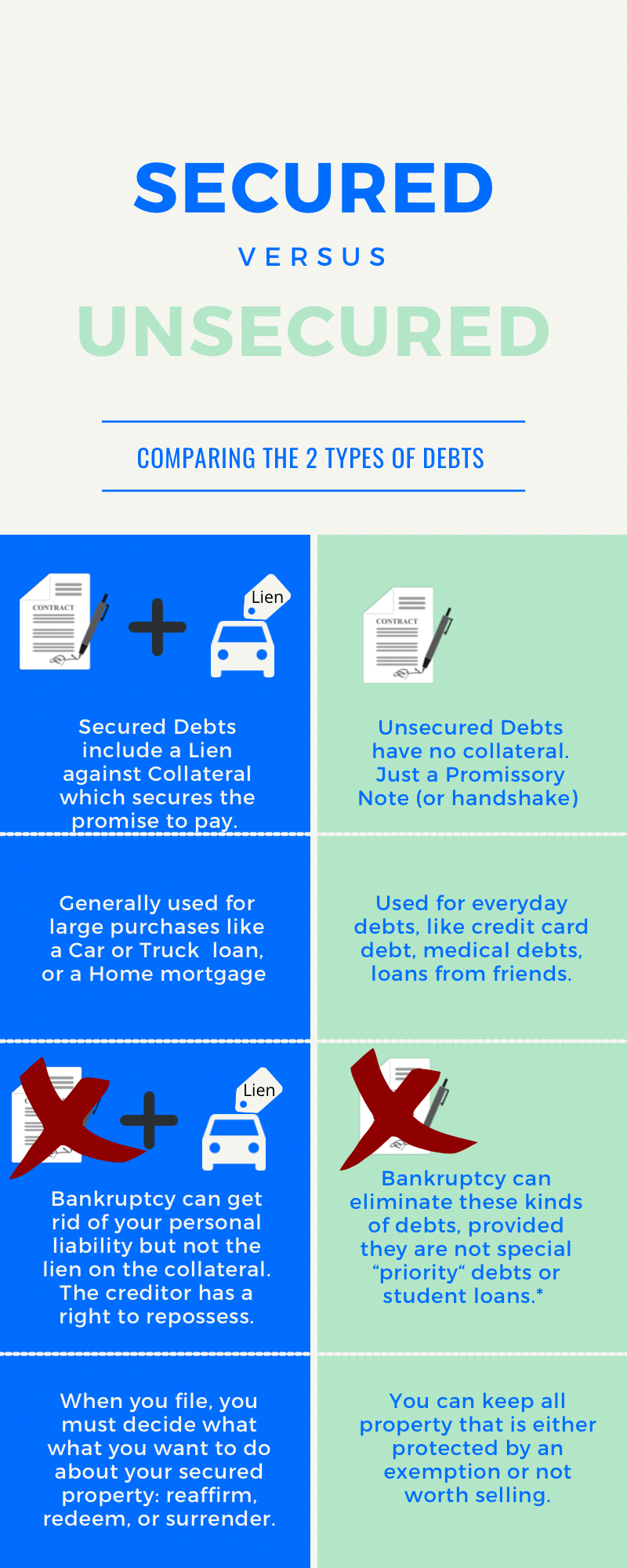

Secured debt. A secured debt is backed up by property, like your home or a car, also known as "collateral." The creditor can take back the collateral if you don't repay the debt.

Secured debt can be voluntary -- for example, when you get a mortgage to buy real estate or a car loan. It can also be involuntary -- say, if the government puts a lien on your property for back taxes.

Unsecured debt. Unsecured debt isn't backed up by collateral. Lenders give you credit without "security," relying on your credit history and your promise to repay. Unsecured debt can include everything from your credit cards to your gym membership, your medical bills to a loan from a friend.

In bankruptcy, unsecured debt is divided into priority and non-priority claims. If there's any money available to pay your creditors, priority claims come first. Non-priority unsecured debts are rarely paid in bankruptcy.

Common priority unsecured debts include:

- legal fees related to the bankruptcy filing

- child support and alimony

- federal or state income taxes

- a certain amount of wages and benefits owed to employees, and

- claims against you for operating a vehicle under the influence of alcohol or drugs.

To learn more, see our articles on How to File for Bankruptcy.