Quick Answer:

Most people who file for bankruptcy can end up keeping their car or at least some kind of vehicle that can get them to work and back, but the answer depends on your particular circumstances and the laws of your state.

If you’re leasing your car

If you’re leasing your car, it’s between you and your lessor whether you want to keep making payments on the lease or make arrangements to give up the car.

You’ll be asked to list your leases and what you intend to do about them on Form 106.

If you own your car free and clear

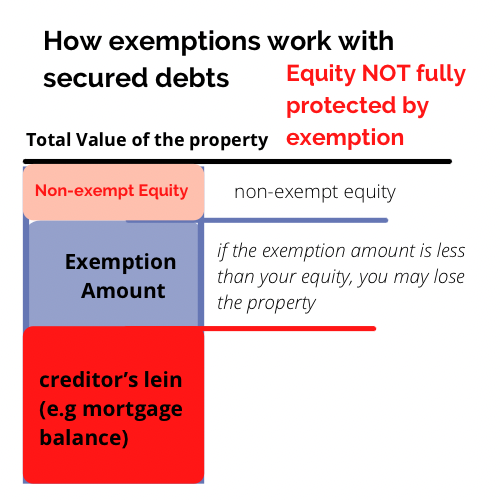

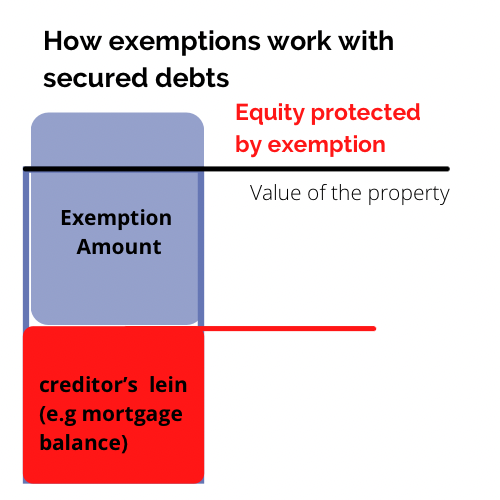

If you own your car free and clear, you will be allowed to keep it as long as:

- its current value

- is less than the available exemption amount available in your state.

- If you have a vehicle (e.g., a truck or a van that is a “tool of trade” for your work or business, you may have additional exemption options. See Tools of Trade Exemptions.

If you still have a car loan

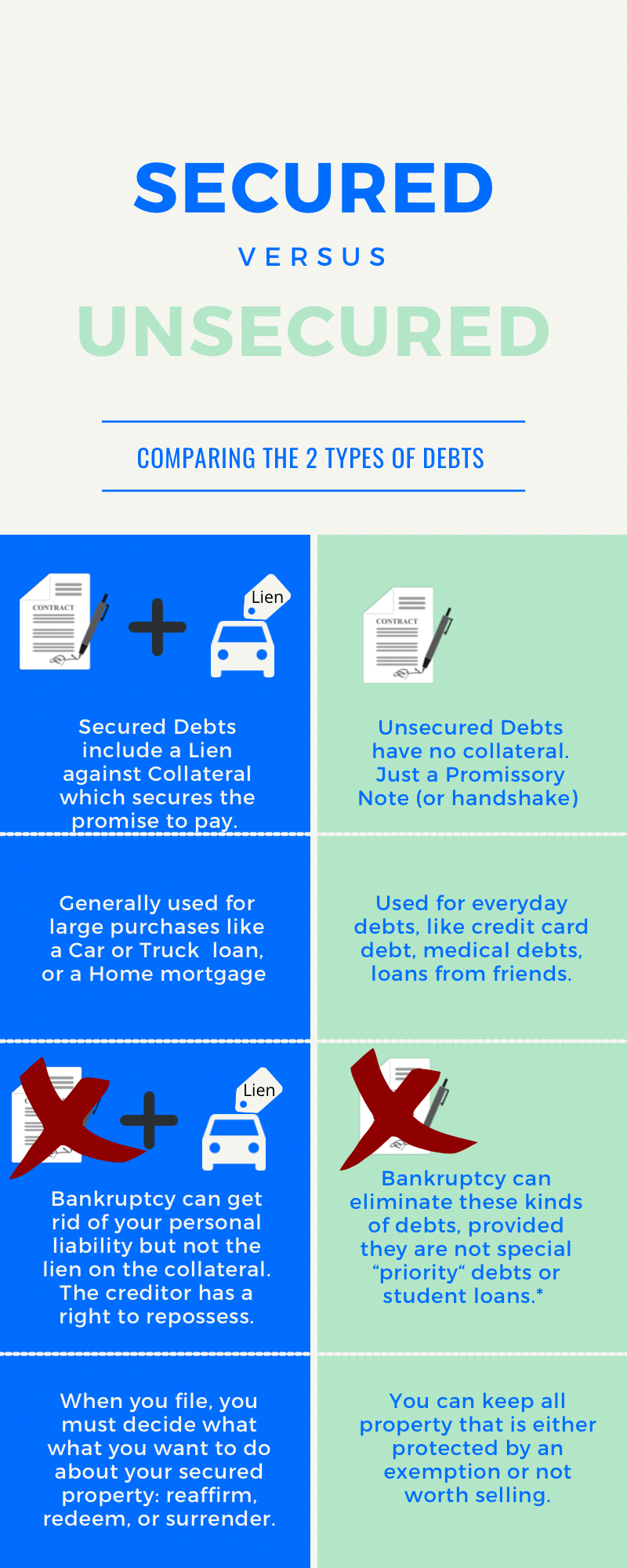

If you still have a car loan, your bankruptcy will wipe out your personal liability for your car note, but the lien on your car will remain:

As with all secured debts in bankruptcy, a secured car loan consists of two parts:

- a promissory note - attached to you - holding you "personally liable" for the loan amount

(your "bankruptcy discharge" wipes this out)- a lien - attached to the vehicle - allowing the lender to foreclose and take the vehicle if you don't pay your promissory note

(this part is unaffected by your "bankruptcy discharge"—because it's attached to the property, not to you...)

Reaffirm? Redeem? Surrender? Ride Through?

If you file for bankruptcy, you’ll be asked what you want to do about your car loan on the “Statement of Intention” form (Form 108)

- Choose to keep the car, and

- reaffirm your personal liability on the debt, via a “reaffirmation agreement with the lender — which keeps you responsible for the debt, despite your bankruptcy.

- Or redeem the property by paying its current value to the creditor, done and done.

- Surrender it back to the car lender, and

- wait for the lender to come to pick it up (get the keys or tow it), or

- ...or “ride through” by making monthly payments on the property as long as the creditor doesn’t repossess the car — even though you can’t be sued for any personal liability, and hope the creditor lets you keep the car.

(This “informal” practice varies widely across the nation. Talk to a local bankruptcy lawyer to determine the custom in your district. Also, with used cars rising in value, letting debtors retain the vehicle is less common if the used vehicle can be quickly sold in a hot market.)- If you surrender the car, your obligation to pay the car loan is discharged along with your unsecured debts. That’s why creditors may be disinclined to let you “ride through” because if the car stops working or is damaged, you can walk away from it and not owe anything more — and all the creditor may be left with is the damaged or neglected vehicle’s salvage value at the junkyard.

How much could the trustee get for “the bankruptcy estate” if they sold your vehicle?

Would there be anything left after the trustee has paid off:

- the costs of sale

- creditors liens

- your exemption amount

Federal Bankruptcy §522(d) Exemptions for Cars

Some states allow you to use the Federal bankruptcy exemptions under §522(d), which has:

- A motor vehicle exemption limit of $4,000 (11 U.S.C. § 522 (d)(2)), and

- a wild card of $1,325 of any property (11 U.S.C. § 522 (d)(5)), and

- up to an extra $12,575 worth of any property if you don’t use all of the $25,150 federal homestead exemption. (11 U.S.C. § 522 (d)(1), (d)(5))

50 State Vehicle & Wild Card Exemptions:

The table below shows the vehicle and wild card exemptions in state law.

-FURTHER READING:

Chapters 3 and 5 of How to File Chapter 7 Bankruptcy addresses the issue of what happens to your property in a Chapter 7 Bankruptcy

Chapter 3. Your Property and Bankruptcy

- Property in Your Bankruptcy Estate

- Property You Own and Possess

- Property You Own and Don't Possess

- Property You Have Recently Given Away

- Property You Are Entitled to Receive but Don't Yet Possess When You File

- Proceeds From Property of the Bankruptcy Estate

- Certain Property Acquired Within 180 Days After You File

- Your Share of Marital Property

- Property That Isn’t in Your Bankruptcy Estate

- Property You Can Keep (The Exemption System)

- How Exemptions Work

- Applying Exemptions to Your Property

- Selling Nonexempt Property Before You File

- Five Guidelines for Pre-bankruptcy Planning

Chapter 5. Secured Debts

- What Are Secured Debts?

- Security Interests

- Nonconsensual Liens

- What Happens to Secured Debts When You File for Bankruptcy

- Eliminating Liens in Bankruptcy

- If You Don't Eliminate Liens

- Options for Handling Secured Debts in Chapter 7 Bankruptcy

- Option 1: Surrender the Collateral

- Option 2: Redeem the Collateral

- Option 3: Retain and Pay ("Ride Through")

- Option 4: Reaffirm the Debt

- Option 5: Eliminate (Avoid) Liens

- Lien Elimination Techniques Beyond the Scope of This Book

- Choosing the Best Options

- What Property Should You Keep?

- Real Estate and Motor Vehicles

- Exempt Property

- Nonexempt Property

- Step-by-Step Instructions

- How to Surrender Property

- How to Avoid Liens on Exempt Property

- How to Redeem Property

- How to Reaffirm a Debt

How to File Chapter 7 Bankruptcy, (Nolo) by Albin Renauer & Cara O'Neil