What are Bankruptcy Exemptions?

"Exempt" property under bankruptcy law means that it is protected from creditors and cannot be used to satisfy the debtor's debts.

Exemption laws are a key part of bankruptcy's fresh start, designed to give debtors a solid foundation on which to launch their new financial life post bankruptcy.

Protecting Your Assets in Bankruptcy: Property Exemption Laws

Property you get to keep*

The law of what has come to be called "Asset Protection" is actually a mixture of laws that allow you to keep certain property no matter what, even if you owe money to others. Every state has laws that designate specific property you get to keep so that you can continue living a productive life. That is, even if you owe a trillion dollars to someone, the law won't make you sell the shirt off your back to pay it. And in Texas and Florida, they won't even make you sell your million dollar mansion, or in Nevada, your gun.

These rules are called "property exemptions." They vary from state to state. They designate what property is off limits to your 'creditors '-- the legal name for those who claim you owe them money.

What are Bankruptcy Exemptions?

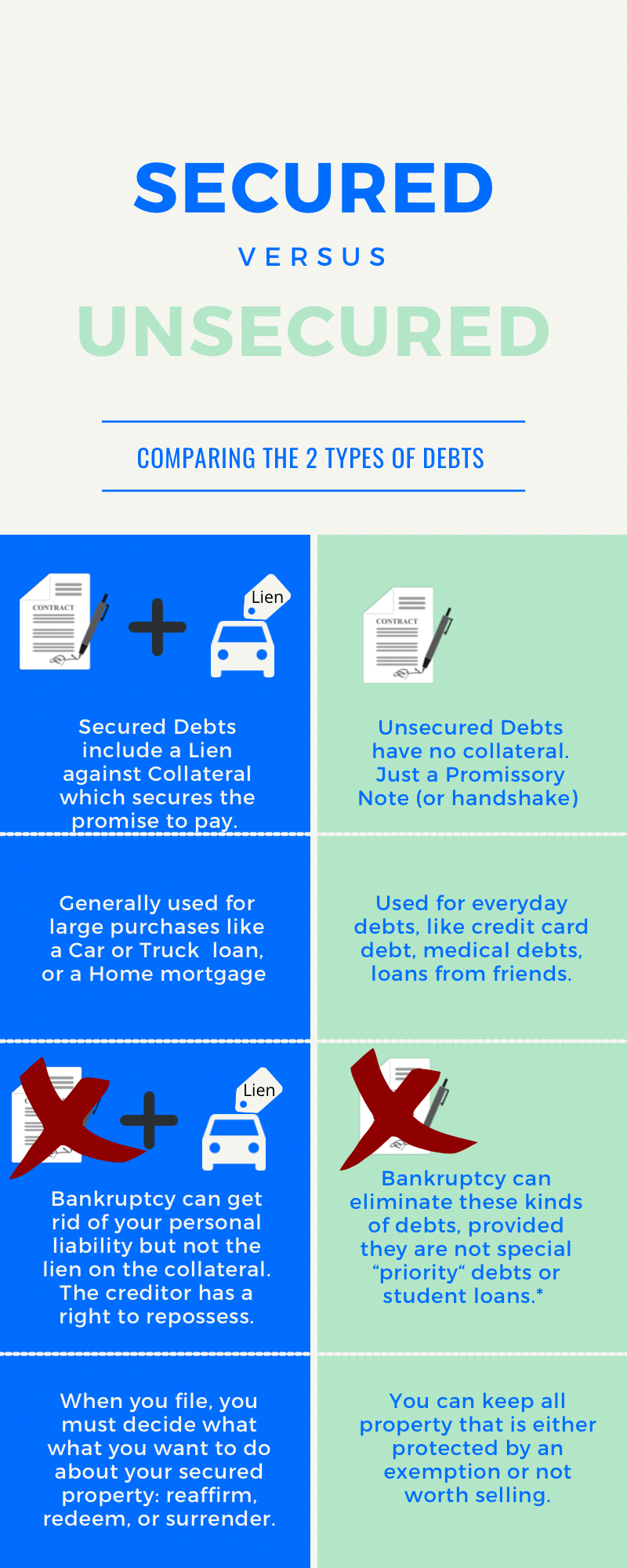

Every state has laws that designate certain types of property (your home, some personal possessions, tools of your trade) that are off-limits to "unsecured" creditors -- that is, creditors who do not have a lien on your property. Credit card debt and medical bills are the two the most common types of unsecured debt (unless you have a special 'secured' credit card).

Unsecured creditors cannot force you to sell your exempt property to pay off the debt. Even if the creditor goes to court wins a court judgment against you, and takes steps to attach a 'judgment lien' to your property, you are still entitled to your exemption amount before any sale proceeds are distributed to the unsecured creditor. (However, some debts, like child support, may be an exception.)

If you eventually do sell your property voluntarily, the creditor has a right to have its lien paid from the sale proceeds before you receive anything.

"No Asset" Bankruptcies

As a practical matter, most people facing bankruptcy only own property that is exempt, and have no interest in selling what they have. If all of your property is protected by exemption laws, you are said to be "judgment proof" -- whether or not you file for bankruptcy.

If you do file for bankruptcy and all your property is exempt, your case is known as a "no asset" bankruptcy--which really means you have no non-exempt assets.

In bankruptcy, a court official called the "bankruptcy trustee" represents the rights of all unsecured creditors. The trustee can assert whatever rights the creditors would have if they had a court judgment against you.

Secured Creditors Have Priority

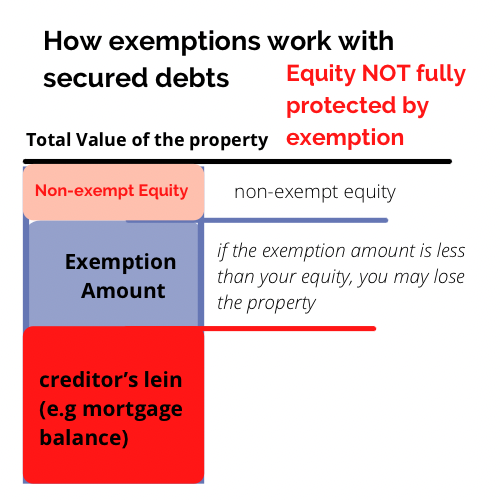

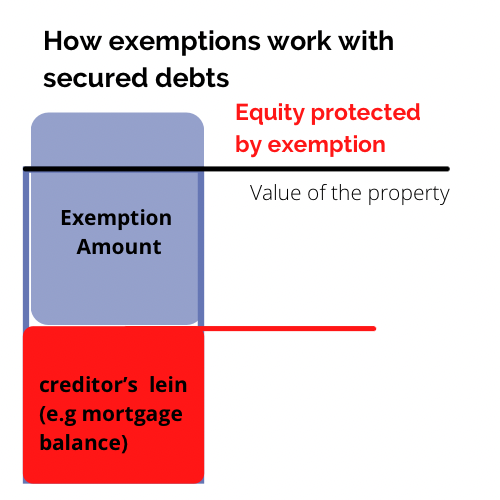

Another important thing to remember about exemptions is that it only protects the "equity" in your property. That is the difference between the value of the property, and what you owe to secured creditors.

If you contractually agreed to pledge your property as collateral for a debt, this property is known as "secured property," and the debt is called a "secured" debt, and the person you owe is a "secured creditor" and they have a "security interest" in the property. If the debt was incurred to purchase the property itself (e.g. a car loan or first mortgage), the creditor is said to have a "purchase money security interest" (PMSI). Exemption laws offer no protection against such contractual agreements that give the creditor a PMSI.

EXAMPLE:

If you owe $10,000 on a $12,000 car, you have only $2,000 in equity. If your state has at least a $2,000 exemption for motor vehicles, that will be enough to protect the car in bankruptcy --(but you'll still need to make the car payments to the secured creditor.

On the other hand, if you own the vehicle free and clear, then your equity is the full value of the vehicle, and a $2,000 exemption would not enough to protect it. The trustee would force the sale of the car, you would get your exemption amount, and the trustee would get the rest of the proceeds to distribute to the unsecured creditors.