If you own a home, Chapter 7 may not be the best option for dealing with your debts. Chapter 13 may be a better option.

If you have significant non-exempt equity in your home, you could lose your house in Chapter 7 bankruptcy, if your state does not have an unlimited or sizable homestead exemption.

And, perhaps more important, Chapter 7 cannot prevent a foreclosure of your home, although Chapter 13 can buy you time, if you need time cure a default to to forestall a foreclosure while you get your financial house in order over the next 3 to 5 years under court supervision.

If you do file Chapter 7, you’ll need to keep current on your mortgage payments and make sure all of your equity is protected by exemptions before you file.

NOTE: This topic is complex enough that an entire thirty-page fourth chapter of my book is devoted to just this topic. See, Chapter 4 of How to File For Chapter 7 Bankruptcy, (Nolo 2021, 22nd ed.) That chapter discusses what happens if you file for bankruptcy, as well as what options you have outside of bankruptcy to deal with mortgages, such as mortgage modifications. Those topics are beyond the scope of this website.

Consult with an experienced bankruptcy attorney in your state who is familiar with State foreclosure and exemption laws to know all of your options and consequences before you file.

NOTE - IF YOU RENT: If you rent your home, completely different considerations apply. Bankruptcy cannot provide much protection against an eviction (a delay at most) so you should plan to keep current on rent if you file for bankruptcy. Some people use bankruptcy to make sure they have enough rent money, by using bankruptcy laws to eliminate other types of debts (like medical debt and credit card bills) that bankruptcy can deal with.

What Will Happen to My House?

The laws of mortgages, competing liens, and secured debts and property exemptions vary from state to state, and can be tricky for the novice who has never navigated the layers of overlapping rules and procedures that govern you keeping your house.

Will the Trustee Take Your Home and Sell It?

It depends on your particular facts. Everyone’s facts are different.

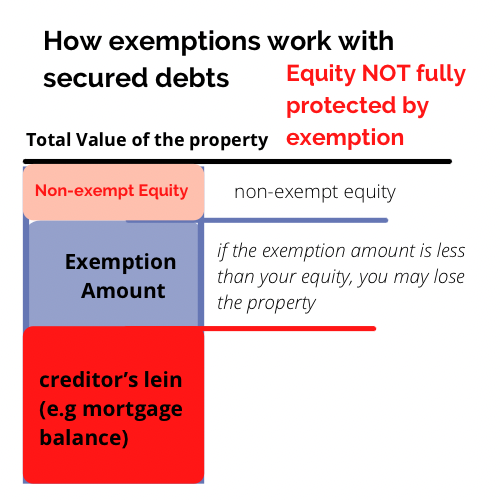

The trustee will go after you house IF there is any non-exempt equity left in your home.

Non-exempt Equity is what's left, after paying off:

- what you owe on any mortgages,

- your exemption amount, (in your state -- and California and Washington, your county)

- any other non-voidable liens, and

- the costs of sale

The trustee's goal is to raise money for unsecured creditors.... If there's nothing left to be had from your house for unsecured credtors, the trustee will "abandon" the property.. that is, no longer include it in the "bankruptcy estate" from which the trustee can draw funds to pay unsecured creditors.

Factors to consider if you file for Chapter 7:

Are you current on your mortgage?

If you're behind on your mortgage and facing foreclosure, you may want to consider Chapter 13, especially if your home equity is not completely protected by an exemption in your state.

A Chapter 7 bankruptcy cannot stop a lender from foreclosing on your house, but a Chapter 13 bankruptcy can. In fact, preventing foreclosure is a major reason people end up filing Chapter 13 bankruptcy (rather than Chapter 7) if they are in such a situation, because Chapter 13 law has specific provisions designed to help cure mortgage arrears or deal with large balloon payments by spreading them over a five year repayment plan, rather than all at once.

What Happens to Your Mortgage in Chapter 7 Bankruptcy?

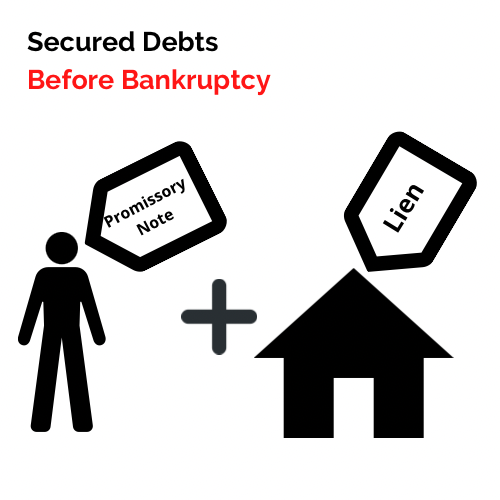

Like any "secured debt," a mortgage or deed of trust consists of two parts:

- A promissory note, (the contract to pay) and

- A lien. (the 'security' that the lender can go after in case you don't pay)

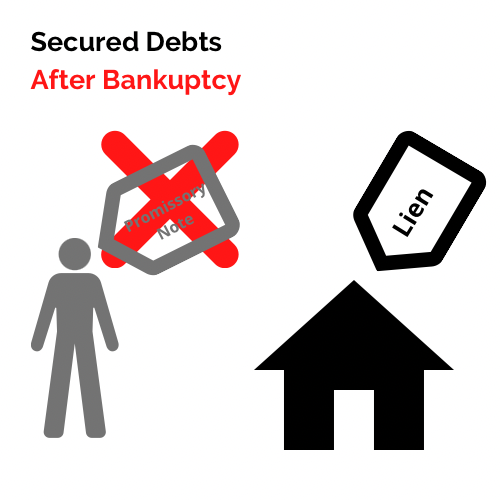

Bankruptcy, eliminates your personal liability for a secured loan, but leaves the lien intact

The promissory note "attaches" to YOU, and makes YOU personally liable for paying off the debt.

The lien (also known as a "security interest") "attaches" to the PROPERTY, and makes the property liable for the debt.

Because the lien is attached to the property, it stays with any transfer of the property, and is unaffected by your bankruptcy discharge.

And if the property is sold or given away, the property is still liable for the debt, and generally those debts must be paid in full before the property is transferred in a sale.

Note: Having no personal liablity can cause problems if you want loan modification later.

How much of your home equity is protected by your state’s homestead exemption?

Equity, Exemptions and Secured Debts in Bankruptcy

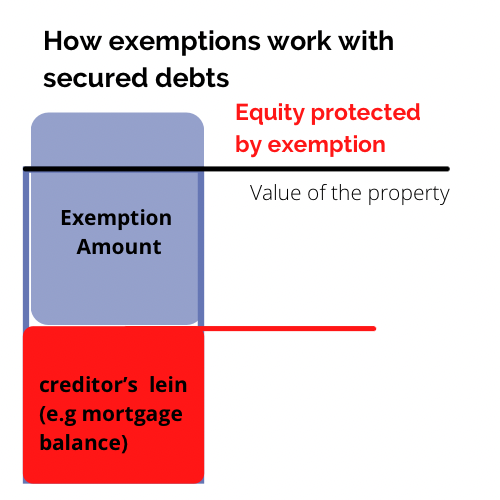

The equity in your home is:

- the total value of your home,

- minus secured debts and liens against it.

Unless your equity is fully protected by a bankruptcy exemption you can use, the trustee might take it

Federal Homestead Exemption

If your state allows you to use the federal bankruptcy exemptions in section 522(d) of the bankruptcy code, then you can protect $27,900 of home equity under the federal bankruptcy exemptions — less than most states protect these days.

50 State Homestead Exemptions

State laws vary widely in the amount of equity they protect in a home, from the unlimited exemptions in Florida, Texas, Oklahoma, ___ and others, (see chart) to the measly $300 homestead exemption in Pennsylvania.

Most states exemptions are less than $100,000 in equity.

However, every year. more and more states have increased their homestead exemptions with states like Nevada, California, Minnesota, Connecticut, Massachusetts and others allowing you to shield hundreds of thousands of dollars of home equity from the reach of the bankruptcy trustee.

Are there liens on you home that the trustee could eliminate and create non-exempt equity?

Even if you may think that your home is "under water" (that is, has no equity because the cumulative amount of liens on your home exceed its value), you should be aware that some kinds of liens can possibly be eliminated in bankruptcy.

And sometimes a trustee will look for such "defective" liens (for example, if there was some technical flaw in the recording of the lien), and will attempt to "void" such a lien (via a process called "lien avoidance") to free up non-exempt equity in your home that could be used to pay your unsecured creditors. (Remember, bankruptcy trustees earn a commission on any amounts they distribute to unsecured creditors, so they are motivated to find and liquidate such assets. Indeed, it's their job.)

Find an experienced attorney with knowledge of local property and foreclosure laws who can look at your particular situation and let you know where you stand on these issues.

FURTHER READING:

Chapter 4 of How to File Chapter 7 Bankruptcy addresses the issue of what happens to your house in a Chapter 7 Bankruptcy

- How Bankruptcy Affects a Typical Homeowner

- Mortgage Payments

- Liens on Your House

- Keeping Your House

- If You’re Behind on Your Mortgage Payments

- Negotiating With the Lender

- Mortgage Modifications

- If the Lender Starts to Foreclose

- Defenses to Foreclosure

- If Foreclosure is Unavoidable

- Will You Lose Your Home?